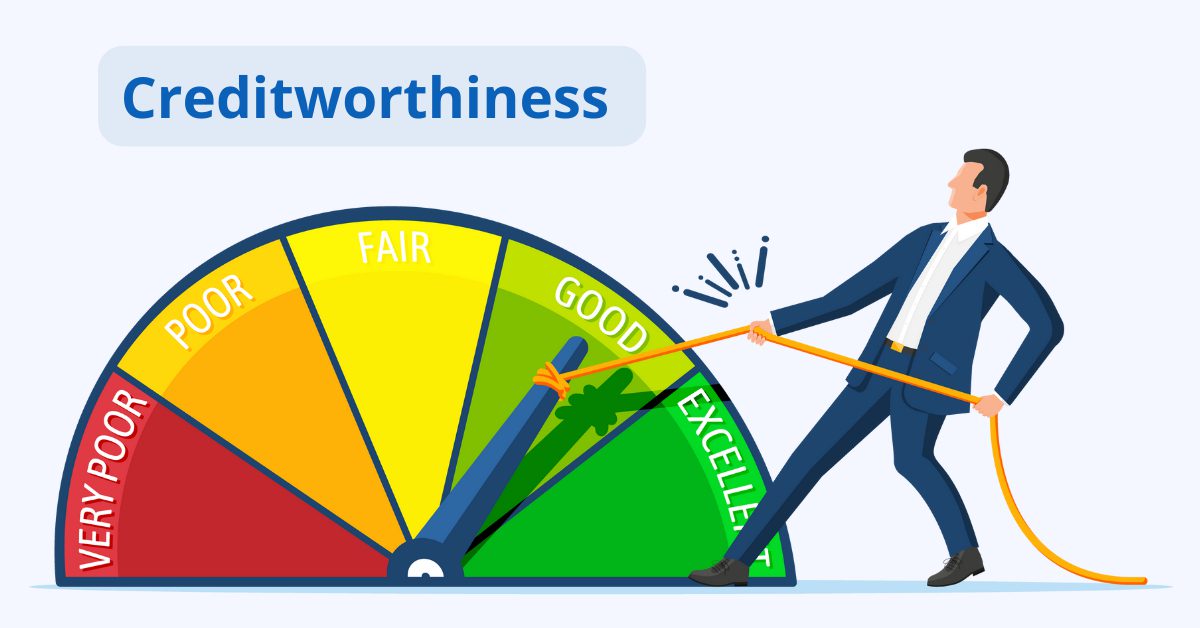

Your financial health is not just about the money you have in your bank account or the loans you take; it’s also about your creditworthiness. And in the realm of creditworthiness, the CIBIL Score reigns supreme. However, many individuals lack knowledge about this mysterious number and often make common mistakes that impact their CIBIL Score. In this article, we will unravel the secrets of CIBIL Scores and shed light on the errors you should avoid to maintain a healthy credit profile.

Lack of Knowledge on CIBIL Score:

One of the primary mistakes people make is not understanding what a CIBIL Score is and how it affects their financial standing. Your CIBIL Score is a three-digit number that ranges from 300 to 900, reflecting your creditworthiness. Ignorance about its significance can lead to inadvertent errors that harm your score.

Using cash withdrawal from credit card:

In today’s digital age, relying on cash transactions might seem harmless. However, excessive use of cash can limit your credit exposure, as it leaves no traceable record of your financial behavior. Lenders prefer individuals with a history of responsible credit usage, so make sure to use credit wisely and maintain a healthy mix of credit types.

Using Above Limit Credit:

Maxing out your credit cards or utilizing a large portion of your credit limit can have adverse effects on your CIBIL Score. It signals a high credit utilization ratio, which suggests a dependency on credit and raises concerns about your ability to manage debts responsibly. Strive to keep your credit utilization below 70% of the available limit.

Exhausting Over Limit:

Similar to using above limit credit, exceeding your credit limit is a red flag for lenders. It indicates a lack of financial discipline and can significantly impact your CIBIL Score. Ensure that you monitor your credit card balances closely and avoid crossing the prescribed limits.

Suddenly Decreasing Credit Usage:

While excessive credit usage can hurt your CIBIL Score, abruptly reducing your credit usage can also have unintended consequences. Lenders assess your credit behavior over time, and a sudden drop in credit activity may create doubts about your creditworthiness. Maintain a balanced approach by using credit responsibly and consistently.

Outdated CIBIL Score Websites:

The digital era comes with its fair share of technical glitches. CIBIL scores can be affected if the official websites are not updated regularly. It is crucial to rely on accurate and up-to-date information when monitoring your CIBIL Score. Ensure you access your score from trusted sources to stay informed about your credit health.

Not Knowing the Procedures:

Lastly, not knowing the procedures for rectifying errors or discrepancies in your credit report can prove detrimental. Inaccurate information can drag down your CIBIL Score, so it’s vital to familiarize yourself with the dispute resolution process. Stay proactive and regularly review your credit report to address any issues promptly.

Conclusion:

Your CIBIL Score is a critical aspect of your financial journey, impacting your ability to secure loans, favorable interest rates, and various financial opportunities. By avoiding these common mistakes and being proactive in managing your credit, you can ensure a healthy CIBIL Score. Educate yourself about credit practices, monitor your credit utilization, and stay updated on your credit report to unlock the doors to financial success.

Remember, a strong CIBIL Score reflects responsible credit behavior and opens doors to better financial prospects. Empower yourself with knowledge, make informed decisions, and watch your creditworthiness soar.